As the Housing Bubble/Credit Crisis collapses, WHAT SHOULD BE DONE ?

As the Housing Bubble/Credit Crisis collapses, WHAT SHOULD BE DONE ?

According to a 13 March 2008 article by Damian Reece on Telegraph.co.uk:

"… The Fed, with its latest $200bn [billion] offer of cheap cash, has provided yet more state aid for errant hedge funds and another Washington-backed bail-out for Wall Street bankers … The Fed has saved the day again, but it will only be for a day or so…We have not seen anything like it since the decade of the Great Depression. …

How much further can the central banks go to support a system that is so obviously broken? …".

According to a 14 March 2008 article by Ambrose Evans-Pritchard on Telegraph.co.uk:

"… The market was starting to question the solvency of bodies that stand at the top of the credit pile. These agencies together wrap or insure $6 trillion of mortgages. …".

A 13 March 2008 politicallore.com web post by Alexander Nobles quoted Ron Paul as saying:

"... Since the Fed stopped publishing M3, which tracks the total supply of dollars in the economy, we can't even be sure how many dollars they are creating.Reported inflation is around 2%, but the method for calculating inflation changed in the 1980's, largely at Mr. Greenspan's urging. Private economists using the original method find actual inflation to be over 10 per cent ...".

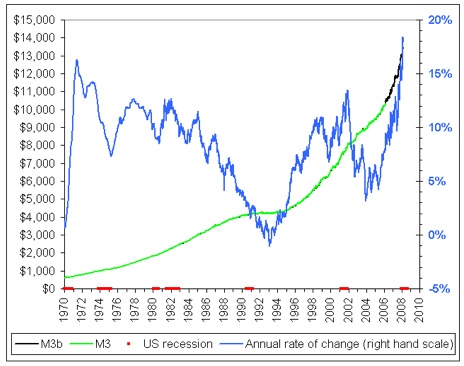

According to a nowandfutures.com web page:

"... We did some sleuthing and data extraction and put M3 back together [denoted M3b] from various weekly Federal Reserve reports that are still available. ... Ours tends to be more volatile and averages slightly higher than ...[the]... monthly reconstruction of M3 ...[by]... John Williams ...".

The nowandfutures.com M3 graph of "update 3/07/08" shown above indicates:

Back in 1988-1992 when Bush I was USA President, the Money Supply (USA dollars in the world) was around $4 trillion and the Rate of Change was near zero.

In 1992 Bill Clinton was elected using the slogan "It's the Economy, stupid", and during his terms 1992-2000 the Money Supply grew from $4 trillion to $7 trillion.

The $3 trillion of new money in the Clinton era funded a Dot-Com boom bubble that burst around 2000, when Bush II became USA President. As with all booms, some Dot-Com assets survived, so maybe about $1 trillion remained in the Dot-Com sector with $2 trillion collapse-money seeking to flow to some other sector.

In the first term (2000-2004) of Bush II included the 9/11 destruction of the Twin Towers and the beginning of the Iraq War, but the dominant economic force was

the flow of money from collapsed Dot-Com assets into a Mortgage Bubble based on housing construction funded by banks who created complex securites based on mortgages and sold them to Hedge-Fundies.

The securitization process insulated the banks from risk, so the banks could and did lend to everybody who asked for money, without regard to credit-worthiness.

The securitization process was so complex that the Hedge-Fundies could and did easily hide the probability of risk from their investors.

As long as the Mortgage Bubble continued to grow faster than problems arose, the builders, bankers, and Hedge-Fundies, and their insurers, were very happy sharing the Bubble Money:

During the first half (2004-2006) of the second term of Bush II, the Money Supply increased another $1 trillion to $10 trillion,

but the occupation phase of the Iraq War turned out to be much more difficult and expensive than Bush II had anticipated, so most of the new $1 trillion went to the Iraq Was instead of pumping up the Mortgage Bubble.

To make the builders, bankers, Hedge-Fundies, and insurers happy, AND to fund the occupation phase of the Iraq War (like Lyndon Johnson's Guns and Butter policy with respect to the 1960s Vietnam War and Great Society), Bush II saw that the Money Supply would have to be increased greatly, and indeed from 2006 to now (March 2008) the Rate of Change went from about +5 per cent to + 18 per cent and the Money Supply went from $10 trillion to almost $14 trillion.

Bush II did not want to appear grossly inflationary, and tried to avoid doing so by

Where did the $4 trillion created by Bush II since 2006 go ?

Some of it went to the Iraq War, but my guess is that no more than $1 trillion.

Another $2 trillion can be accounted for by adding another$2 trillion to the Clinton $2 trillion and the Bush II first-term $2 trillion puts the Mortgage Bubble size at the $6 trillion figure mentioned by Ambrose Evans-Pritchard as the amount of mortgages covered by USA agencies.

The remaining $1 trillion may have gone to parts of the Mortgage Bubble not covered by those USA agencies, so that:

Of course, all the Mortgages are not bad, so some of the $8 trillion Mortgage Bubble is sound, so maybe a useful guess might be that the bad part might be about $3 trillion. If so, such a

USA Government projects producing more economic growth than they cost include:

One of those, Nuclear Energy, is not only useful in the short term due to the eminent Depletion of Cheap Oil, but is also useful in the long term. Using Nuclear Reactors to produce energy and hydrogen fuel and to desalt sea water would solve a lot of problems of the world.

Manufacturing and maintaining the reactors could re-establish the USA as a manufacturing power.

To avoid the risk of short-term capitalist greed outsourcing the jobs and factories related to Nuclear Energy, the project should be, like the Interstate Highway System, a USA Government project:

Now (March 2008) the world has $14 trillion USA, of wihich about $7 trillion are related to mortgages, but:

how much does the total $14 trillion get increased by leverage multiplication ?

how secure/risky are the leveraged assets ?

According to a 17 March 2008 Time web article by Janet Morrissey:

the ... mortgage market ...is valued at about .... $7.1 trillion ...

the U. S. stock market ... is valued at about $22 trillion ...

according to the International Swaps and Derivatives Association ... in mid-2007 ... The CDS market exploded over the past decade to more than $45 trillion ...

Credit default swaps are insurance-like contracts that promise to cover losses on certain securities in the event of a default ... commercial banks are among the most active in this market, with the top 25 banks holding more than $13 trillion in credit default swaps ...".

So,

How fast did that happen?

According to a 23 March 2008 New York Times web article by Gretchen Morgenson: "... The value of the insurance outstanding stood at $43 trillion last June, according to the Bank for International Settlements. Two years earlier, that amount was $10.2 trillion. ...".

According to a 23 March 2008 New York Time web article by Nelson D. Schwartz and Julie Creswell: "... Today, the outstanding value of the swaps stands at more than $45.5 trillion, up from $900 billion in 2001. ...".

So the leveraged growth of the CDS market has been:

2006 - $10 trillion

2008 - $45 trillion

In other words:

in the 2 years 2006-2008, the CDS market increased by another $35 trillion, rougly 2.5 times the total amount of $USA in the world in 2008.

Current Fed policy may be in agreement:

According to a 23 March 2008 New York Times web article by Gretchen Morgenson:

"... IN the week or so since the Federal Reserve Bank of New York pushed Bear Stearns into the arms of JPMorgan Chase, there has been much buzz about why the deal went down precisely as it did. ... it could be simple coincidence that the rescues caused billions of dollars (or more) in credit insurance on the debt of ... Bear Stearns to become worthless ... Yet an effect ... is the elimination of all outstanding credit default swaps on ... Bear Stearns ...

Entities who wrote the insurance - and would have been required to pay out if the companies defaulted - are the big winners. They can breathe a sigh of relief, pocket the premiums they earned on the insurance and live to play another day.

Investors who bought credit insurance to hedge their Bear Stearns ... bonds will be happy to receive new debt obligations from the acquirers in exchange for their stakes. They are simply out the premiums they paid to buy the insurance.

On the other hand, the big losers here are those who bought the insurance to speculate against the fortunes of two troubled companies. That's because the value of their insurance, which increased as the Bear and Countrywide bonds fell, has now collapsed as those bonds have risen to reflect their takeover by stronger banks. We do not yet know who these speculators are, but hedge fund and proprietary trading desks on Wall Street are undoubtedly among them. ...

So consider all those swaggering hedge fund managers and Wall Street proprietary traders who recorded paper gains on their credit insurance bets as the prices of Bear and Countrywide bonds fell. Now they must reverse those gains as a result of the rescues. If they still hold the insurance contracts, they are up a creek - and the Fed just took away their paddles.

An interesting side note: It's likely that JPMorgan, the biggest bank in the credit default swap market, had a good deal of this kind of exposure to Bear Stearns on its books. Absorbing Bear Stearns for a mere $250 million allows JPMorgan to eliminate that risk at a bargain-basement price. JPMorgan declined to comment on the size of its portfolio of credit default swaps. ... speculators on the losing end of such deals don't typically volunteer that they have suffered enormous hits in their portfolios until they are forced to - often when they're on the brink of collapse.

Do[es] the Bear Stearns ... deal... represent a regulatory template? ... Bondholders won, while stockholders and credit insurance owners lost. Although there aren't that many big banks left that are financially sound enough to buy out the next failure, it's a pretty good bet that future rescues will look a lot like these. ...

It's pretty clear that some major losses are floating around out there on busted credit default swap positions. Investors in hedge funds whose managers have boasted recently about their astute swap bets would be wise to ask whether those gains are on paper or in hand.

Hedge fund managers are paid on paper gains, after all, so the question is more than just rhetorical. ...".

that would

According to a 23 March 2008 New York Time web article by Nelson D. Schwartz and Julie Creswell:

"... After all of the write-downs at the banks in June, July and August [2007], we were in a full-fledged credit crisis with C.E.O.'s of top banks running around like headless chickens ...

for 2000-12 showing a sharp decline from August 2007 to a singularity in 2012. ]

... [Now in March 2008] The Federal Reserve not only taken has action unprecedented since the Great Depression - by lending money directly to major investment banks - but also has put taxpayers on the hook for billions of dollars in questionable trades these same bankers made when the good times were rolling. ... things have gone too far ... The investment community has morphed into something beyond banks and something beyond regulation ... the shadow banking system ...

the shadow banking system ... is the private trading of complex instruments ... In the past decade, there has been an explosion in complex derivative instruments, such as collateralized debt obligations and credit default swaps, which were intended primarily to transfer risk. These products are virtually hidden from investors, analysts and regulators, even though they have emerged as one of Wall Street's most outsized profit engines. They don't trade openly on public exchanges, and financial services firms disclose few details about them. ...

analysts say ... a broader reconsideration of derivatives and the shadow banking system is also in order ... Whalen of Institutional Risk Analytics ... says ... "Not all innovation is good ...

or, in the words of Rudyard Kipling in excerpts from The Gods of the Copybook Headings: